By Haddon Libby

With every day that the pandemic continues, more and more businesses fail. According to BankruptcyData.com, Chapter 11 bankruptcies are up 52% through July as compared with last year.

For those remembering the Great Recession of 2009, there were 38 bankruptcies amongst companies with assets of more than $1 billion. Through the first seven months of 2020, 46 companies of that size have failed. Another 157 companies with assets of more than $50 million have declared bankruptcy.

Most experts believe that we are in the early innings of the economic fallout from the pandemic. “As expected, we continue to see significant year-over-year growth in Chapter 11 commercial bankruptcy filings,” said Deirdre O’Connor, managing director of corporate restructuring at Epiq. O’Connor sees companies in transportation, energy and transportation as those most at risk.

Regulators in the United States and around the world have helped reduce the number of bankruptcies by allowing lenders to ‘amend and pretend’. In the past, banking regulators would deem a loan a problem credit with missed payments and require the banks to set-aside funds for anticipated losses on these loans.

Regulations in the past essentially made a bad situation worse by forcing banks to liquidate companies at the worst possible time. In changing regulations and allowing banks to rewrite the loans and keep businesses going, banking regulators are adjusting to these extraordinary times in logical ways. This buys the business, bank and regulators time in hopes of a solution that does not lead to the demise of countless businesses. While the day of reckoning has been delayed for the companies utilizing these extraordinary measures, reducing payments only delays the inevitable for many businesses in the eye of the economic storm.

Some of the most damaged industries have been in transportation. In the United States, more than $58 billion in government loans have been extended to the airlines industry to date with additional funds needed to stave off massive layoffs and failures in this business. Some of the more notable bankruptcies to date have been Aviance, the largest airline in Latin American, and Virgin Atlantic. Virgin Atlantic is 49% owned by Delta Airlines.

Anyone who drove near the Palm Springs Airport in March or April knows why Hertz sought bankruptcy protection.

With fewer people on the road, demand for oil and gas has fallen just when global production kept markets flush with crude. More than thirty oil and gas companies have filed this year with some of the more notable names including Chesapeake Energy, Diamond Offshore Drilling and Ultra Petroleum. Here in California, the California Resource Company, a 2014 spin-off of Occidental Petroleum and holder of 2 million acres of oil and gas, filed for protection.

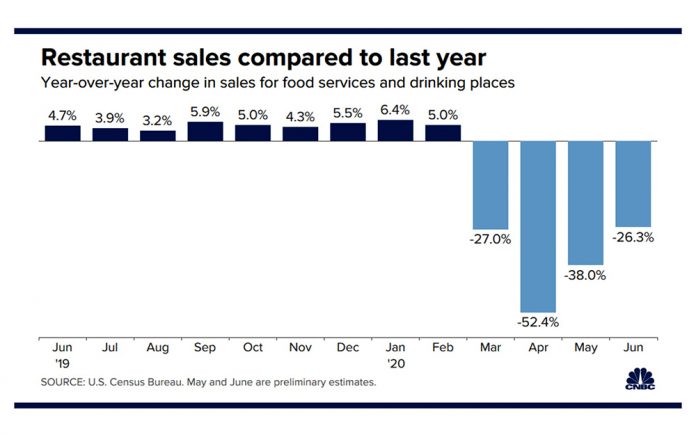

As we all know, the restaurant industry has been savaged. The list of bankruptcies is long and includes well-known chains like California Pizza Kitchen, Souplantation, Sweet Tomato’s, Ruby Tuesday, Red Lobster and Chuck E. Cheese. The owner of 1,200 Pizza Hut and 400 Wendy’s locations has filed with 75% of these locations expected to close.

Retail has also been savaged. Clothiers like Brook Brothers, Men’s Wearhouse and Jos. A Bank have filed. Brands like True Religion, J. Crew, Lucky Brand, New York & Co., Ann Taylor, Lane Bryant and Justice are all in the bankruptcy process. Department stores which were already struggling have seen Neiman Marcus, JC Penney, Lord & Taylor and Stein Mart begin their liquidation process. Specialty stores like Pier 1 Imports, Sur La Table and Tuesday Morning have seen the same fate.

With people unable to go to the gym, 24 Hour Fitness and Gold’s Gym are in bankruptcy protection along with General Nutrition Center (GNC).

In addition to these businesses, real estate investors in commercial as well as residential rentals have seen their cash flows crumble as people stay away from business centers while millions of Americans are delinquent on rent payments.

For all of the carnage amongst these well-known brands, our favorite local businesses seem to close every day. Yelp, the online reviewer, reports that 80,000 businesses were permanently closed on their platform between March 1st and July 25th with few tied to a bankruptcy filing.

Due to the government relief and stimulus sent to Americans over the spring and summer, non-commercial Chapter 13 bankruptcies are down 38% in 2020 to 99,136 reports Epiq. Similarly, Chapter 7 non-commercial filings were off 21% through July.

The pandemic drags on and Congress remains in deadlock over additional relief, expect an increase in non-commercial filings.

All the while, stock markets reach all-time highs.

Haddon Libby is the Founder and Managing Partner of Winslow Drake Investment Management. For more information, please visit www.WinslowDrake.com.

{kind=link}