")

By Haddon Libby

The Coachella Valley has a large population of retirees and nonprofits who rely on interest from fixed income investments for their sustenance. With interest rates being at or near historic lows over the last few years, many have stretched for higher yields by buying investments that they might not have chosen otherwise.

As interest rates start moving higher, many fixed income investments possess the very real risk of a decline in the value over the next few years – something referred to as return-free risk. Return-free risk means that an investor has little to no chance of making money on an investment that they own.

This week I want to help you in understanding a risk that you or someone you care about holds in their investment portfolio. To help you understand my credentials, I have advised bank CEOs and CFOs on how to manage their investment portfolios and currently manage an investment advisory practice that helps individuals and businesses with their investments.

Let’s start simple. Do you know what can happen to the return on a 10 year Treasury bond (currently yielding 2.2%) when rates move up just 0.2% or one-fifth of 1%? The value of that bond goes down by an amount that nearly equals the return of that bond. This means that someone owning this bond earns an effective yield of zero.

As interest rates go up, the interest earned on an intermediate or long-dated bond can be expected to be less than the decline in principal value. Those holding fixed income mutual funds can expect to lose value.

If you hold high yield debt or bonds, this same thing can occur and may be worse. The reason things might be worse is because investors feel less of a need to reach for yield by buying the riskier asset that you are holding. This forces the rate on your investment to go up by even more causing you to lose more in principal value.

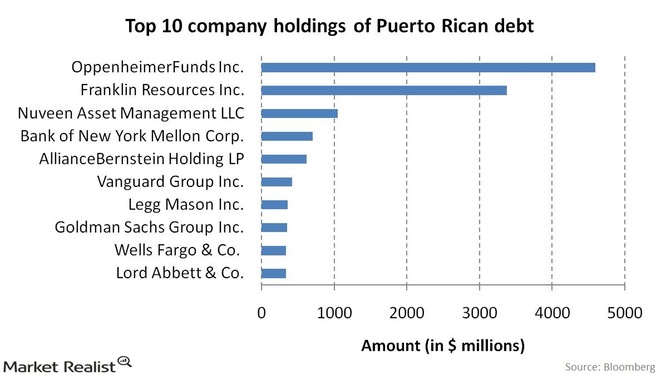

This month’s bond default by Puerto Rico is a great illustration as to how many were taking too much risk. Puerto Rico owes $72 billion, has a 45% poverty rate and does not possess the means to repay its debts. Professional money managers knew this default was coming many years ago yet one in five bond mutual funds held Puerto Rican debt at the time of its default. If you have a fixed income bond fund, there is a reasonable chance that you are at risk. If you hold a Puerto Rican bond outright, you might want to ask your investment advisor why as the crisis in Puerto Rico was not a surprise to anyone.

Another area with potentially more risk than return is International/Emerging Markets debt. Between the fall in oil prices, economic problems in China and a general economic malaise gripping much of the world right now, emerging market debt has more risk than return for the typical investor.

As a general rule of thumb: never invest in something that you do not understand. If an investment advisor gives you verbal assurances on the way an investment is supposed to work, make them back up their words with something in writing that you understand.

If the advisor cannot put their claims and assurances in writing, you should be suspect about their claims as well as the intentions of that advisor. Whether you trust that person or not, always verify all verbal claims. If you don’t know someone who you can truly trust, contact me and I will do a review for you with no expectation of anything in return of any kind.

Haddon Libby is Managing Partner of Winslow Drake, an investment management and advisory firm, and can be reached at hlibby@winslowdrake.com.

{kind=link}