By Haddon Libby

To understand the direction that the economy, equity and bond markets are headed, we need to review basic economics. As we have seen in recent years, the economy does well when government spending is high, companies are investing, workers are employed, and wages are good. Low interest rates help as do tax cuts.

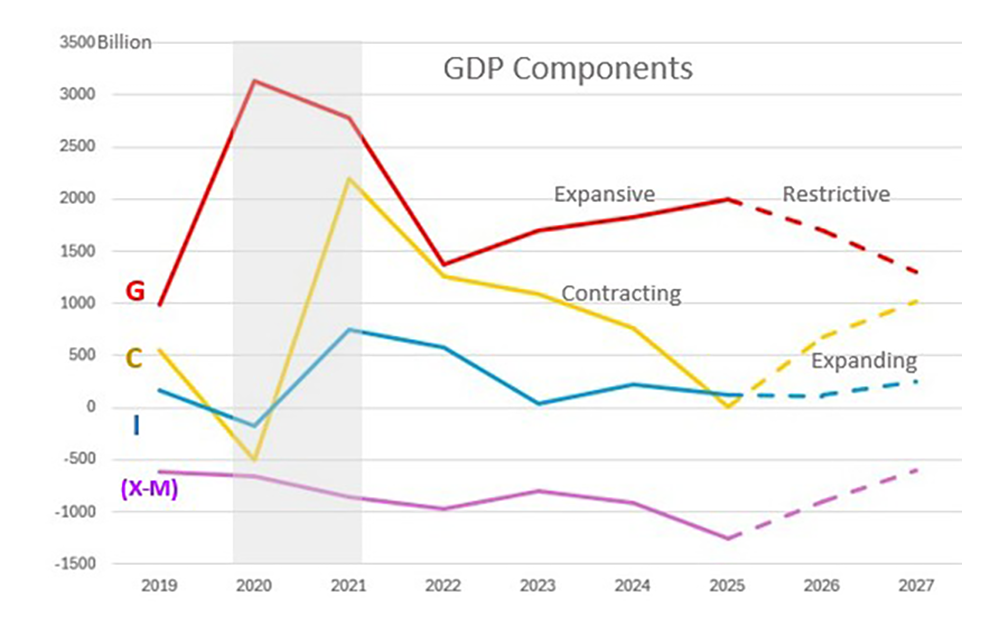

Gross Domestic Product (GDP) is the cornerstone metric for assessing economic performance. For 2025, projections place US GDP at $27 trillion, though analysts anticipate a contraction in the first quarter. GDP is calculated as the sum of Consumer Spending (C), Government Spending (G), Corporate Investment (I), and Net Exports (Exports [X] minus Imports [M]), expressed mathematically as GDP = C + G + I + (X – M). Breaking it down:

- Consumers (C)contribute $19 trillion to GDP. Notably, 22.5% of this ($4.4 trillion) originates from government transfer payments, including Social Security, Medicare, Medicaid, veteran benefits, and unemployment assistance. This reliance underscores the consumer sector’s dependence on public funds.

- Government Spending (G)stands at $5 trillion in direct outlays. If we reclassify consumer-directed transfers as part of G, it surges to $9.4 trillion—over one-third of total US spending. As 2025 began, federal deficits reached $2 trillion annually (7% of GDP), a figure experts consider unsustainable and in desperate need of reduction to avoid long-term damage.

- Investment (I)totals $5.2 trillion, with roughly 20% linked to data center build-outs, fueled by demand for AI and cloud computing. Other significant areas include $1.2 trillion in structures and infrastructure, $1 trillion in intellectual property (e.g., software, movies, research and development), and $1 trillion in equipment purchases by businesses.

- Net Exports (X – M)reveal a record $1.25 trillion deficit, a persistent drag on growth. Key imports include capital goods like computers, consumer goods like automobiles, and industrial supplies like oil. The U.S. imports heavily from Mexico ($475B), China ($440B), and Canada ($420B), while exporting most to Canada ($360B), Mexico ($330B), and China ($155B). Trade imbalances with Germany ($255B in, $63B out) and Japan ($154B in, $66B out) further widen the gap.

The specter of recession looms large. Pre-COVID, deficits approached $1 trillion—double the levels from five years prior. During the pandemic, they skyrocketed by $5.8 trillion (27% of GDP), flooding the economy with cash and igniting inflation as the dollar’s value eroded. Current dynamics highlight the strain:

- Consumers (C), driving two-thirds of GDP, are squeezed by rising prices and stagnant wages, curbing their spending power.

- Government Spending (G)has propped up the economy since 2022, compensating for consumer weakness.

- Investment (I)has tapered off, despite tech-driven data center growth.

- Net Exports (X – M)remain a headwind.

Post-pandemic, spending should have normalized. Outside of recessionary times, deficits typically shouldn’t exceed GDP growth (around 3%, or $1 trillion annually). Instead, they hit $1.4 trillion (5.4% of GDP) in 2022, $1.7 trillion (6.2%) in 2023, $1.8 trillion (6.4%) in 2024, and are projected at $2 trillion (7.2%) in 2025. Such overspending in stable times stokes inflation and jeopardizes future growth. While it staved off a recession in 2022, it’s now a liability..

Deficits must shrink. To avoid a recession from reduced government spending, consumer or investment growth must offset the cuts. Yet, consumers—25% reliant on government programs and 50% driven by the top 20% of earners ($140,000+ households)—face headwinds. Rising unemployment, tied to spending declines, dim hopes for a quick rebound. Without a surge in private activity, 2025 risks a stagflation or a recession as corrective measures needed to solve excessive government spending force a painful correction.

The GOP are hoping that these corrective actions can be accomplished quickly. If not, look for Democrats to have a strong chance to reclaim the House and Senate in 2026 despite highly irresponsible spending over the last three years.

Haddon Libby is the Founder and Chief Investment Officer of Winslow Drake Investment Management, a local Fiduciary RIA firm. For more information on our services, please visit www.WinslowDrake.com.

{kind=link}