By Haddon Libby

The Investment Adviser Association states that Registered Investment Advisory (RIA) firms recently surpassed 1 million employees for the first time. RIA firms manage stocks, bonds and funds for clients. There are 31,700 RIAs in the United States with 16,300 registered with state regulators and 15,400 with the Securities and Exchange Commission (SEC). When a firm manages assets totaling more than $100 million, state regulators oversee these firms. Of those registered with the SEC, 70% have assets under $1 billion.

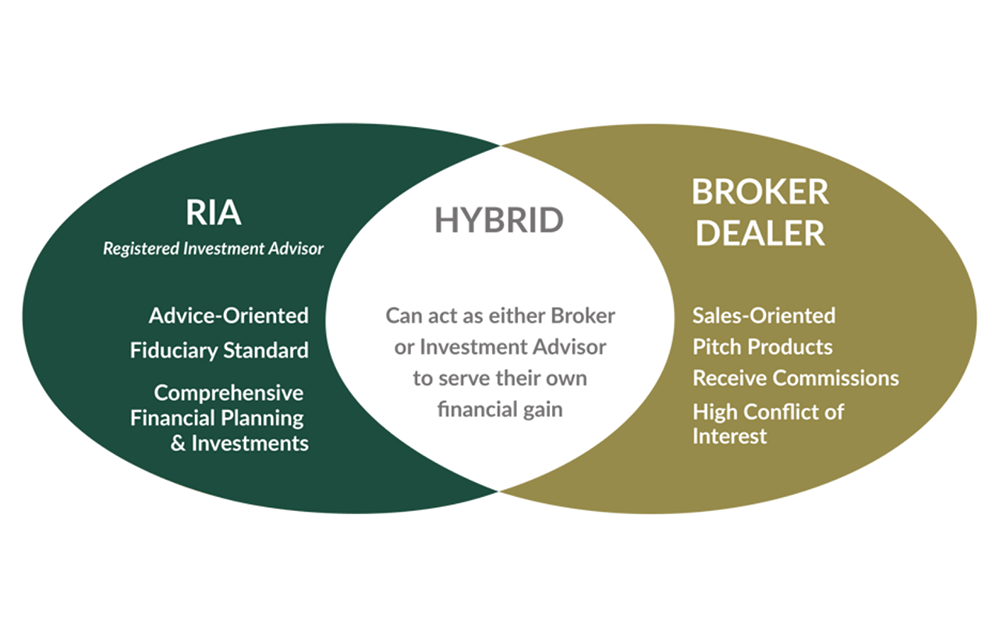

RIAs are different than broker/dealer firms. Broker/Dealer Firms (B/Ds) that you know are Merrill Lynch, Morgan Stanley or Raymond James. My company, Winslow Drake Investment Management, is n state-regulated RIA. There are some firms that try and straddle the fence and refer to themselves as Hybrid firms.

The biggest difference between B/Ds.hybrids and RIAs is the way each are paid. RIAs typically earn income from an asset management fee. For example, if you had a $100,000 account with a RIA, they might charge 1% to earn $1,000 annually. A B/D might also manage your account for 1% to earn $1,000 annually. A B/D can earn more on the purchase or sale of a bond, the placement of a mutual fund in your account, an annuity or private placement. Fees for these products can be as high as 6% to 10%. A hybrid can do all of this.

B/Ds also make money in ways that are seldom disclosed to clients. For example, if the B/D sells enough of the mutual funds from a specific provider, that mutual fund company will pay the B/D a bonus for having client funds in its mutual funds. These fund companies will also pay for additional funds for marketing support. Hybrids may or may not.

One of the most important differences is that an RIA firm typically performs to the Fiduciary Standard. This means that they must put the client first in everything that they do. If the RIA puts its interests ahead of the client, it can get in a lot of trouble.

The typical RIA firm has under ten employees. The firm is usually established by someone looking to break away from B/Ds in order to provide a better service at a better price.

Clients are noticing the difference as the growth rate of RIA firms has been just under 13% over the last ten years versus B/D firms which have grown at an 8% rate.

Let’s look at the RIA firm that I started ten years ago, Winslow Drake Investment Management. I started this after working as an investment banker for 13 years. Following the birth of my daughter in 2001, I moved to the desert to run Bank of America’s Private Bank. After serving as a bank CFO and a few other positions in banking, I started Winslow Drake with one of my best friends in the banking industry.

In starting Winslow Drake, I knew that it was the only way that I could provide the type of service that I wanted to. My goal was to build a small practice that treated everyone the way I would like to be treated when it comes to the management of my money.

The big difference is that we educate our clients on the reasoning behind the purchase or sale of an investment. We help with planning for retirement and serve as a sounding board or advisor to other parts of their financial life. The goal is to be the trusted advisor of my clients. As I work for a fee that is disclosed each month, clients never need to fear that there is a profit incentive in my advice.

This simple act of treating people the way that we would like to be treated has led to awards.

To learn more about the differences between an RIA or B/D firm, sit down with each and compare.

Haddon Libby is the Founder and Chief Investment Officer of Winslow Drake Investment Management, an RIA firm. For more information, please visit www.WinslowDrake.com.

{kind=link}