Celebrates 10th Annual AMP SUMMER CAMP MUSICAL EXTRAVAGANZA!")

")

’ TO FANTASY SPRINGS RESORT CASINO ON DEC. 6, 2024")

By Haddon Libby

Despite a global pandemic and a barely functional two-party government system in Washington DC, US equities have nearly doubled in value while home, food and gas prices are through the roof.

What is going on?

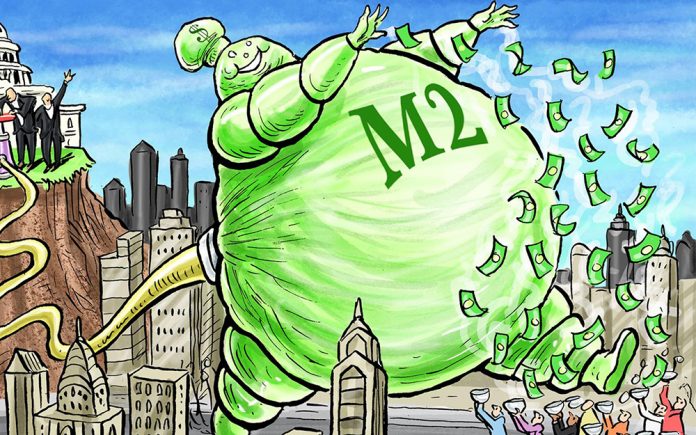

These remarkable returns are largely due to a change in approach by the government in how it goes about stimulating the economy during a massive disruption like the pandemic. The pandemic forced the Federal Reserve and US Treasury to flood the markets with liquidity (aka cash). Since the pandemic started, the US money supply has grown by 30%. Additional cash has been infused into households and businesses to keep the fabric of our economy and our way of life together.

While some money has been in the form of higher unemployment payments, PPP grants and loans, one of the biggest ways that they government has kept the economy together is through low interest rates.

Think about it for a second. We have the highest levels of debt ever yet interest rates are at historic lows. Surely, government intervention is causing markets to behave in an atypical way, right?

What happened is that the Federal Reserve ballooned its balance sheet by nearly $5 trillion through large purchases of Treasuries, Mortgage-Backed Securities (MBS), corporate bond and corporate bond funds. Until this week, the Fed was still buying $30 billion in Treasuries and MBS each WEEK. Beginning this week, purchases are halved to $15 billion per week with expectations for the end of this program next summer.

By keeping interest rates exceptionally low, the Fed is making it easier for borrowers to pay their bills. As Uncle Sam is the biggest borrower (and lender), it is unlikely that we will be seeing rates move significantly higher anytime soon. As the Federal Reserve and Biden Administration continue to promote easy money policies meant to help the people and businesses most impacted by the pandemic, we are seeing inflation.

When inflation is higher than the cost of borrowing money, you have something called Negative Real Rates. The Fed has stated that it is its intent to keep rates low like this for at least another few years.

Let’s pretend that inflation is 5% – an inflation level that is significantly lower than we have today. If you borrow at 2% and inflation is at 5%, your real cost of money is a negative 3%.

What this means is that the cost to repay the debt tomorrow is less than the cost of repaying that debt today. Essentially, the lender is subsidizing the borrower as the underlying currency is worth less tomorrow than it is today. Economists and academics refer to this as a negative real cost of money.

For the person borrowing $300,000 for a residence, the negative real cost of money means that they are saving or making money every year that goes by. If we estimate that the average borrower is paying 3.5% for their mortgage where they would otherwise be paying 6%, that 2.5% in savings is benefitting the homeowner by $7,500 each year. At the same time, the home is appreciating in value causing a double benefit to the property owner.

If you take this math and apply it to multinational corporations, this same impact is being happening making this the best of times for those minimally impacted by the pandemic. This Roaring Twenties type of economic party for some is required to help those most impacted by the pandemic as they begin to rebuild.

Real assets like gas, food, housing and equities tend to go up when the value of the currency goes down. When you add to that the power of negative real rates, you can see why some of finding these to be the best of financial times.

Haddon Libby is the Founder and Chief Investment Officer of award-winning Winslow Drake Investment Management. For a free review of your investment portfolio, please email me at hlibby@winslowdrake.com. For more information, please visit www.WinslowDrake.com.

{kind=link}